Getting Married?

Register Antenuptial Contract R1550 -Easy Online Application.

We have assisted thousands of couples with the registration of their Antenuptial Contracts.

Louwrens Koen Attorneys

Tel: 0870010733 E-Mail: info@louwrenskoen.co.za

YOUR MARITAL REGIME CHOICES BEFORE GETTING MARRIED - different antenuptial contracts compared

Explore your matrimonial property regime options before getting married. You must choose one before getting married. Your choice will have financial and legal consequences. You are therefore urged to carefully consider your options. If you still have questions message us or book a free 20 min consultation with our attorney. Get Started - Explore your options.

Getting Married? Reasons Why you should register an antenuptial contract. R1450 All-Inc

If convinced - Apply Online - R1450 - We have already assisted thousands of couples with the registration of their marriage contracts.

The most common benefits of a marriage out of community of property are as follows:

- The parties will not be held liable for the debts of a spouse that such spouse may have incurred before the marriage;

- The parties will not be held liable for the debts of a spouse that such spouse may incur during the marriage.

- Assets may be protected, particularly if one of the spouses has a business in their own name. The parties may decide to register assets such as their residential property in the name of only one spouse, the spouse with the lowest risk profile. The assets of each spouse will also be safe if their spouse is sequestrated.

- One or both spouses may have assets prior to marriage that they want to exclude from the joint estate.

- Spouses may enter into commercial transactions without the consent of their spouse.

- Each spouse retains control over his or her assets.

LINKS - APPLY ONLINE

- EXPLORE YOUR MARITAL REGIME OPTION BEFORE GETTING MARRIED

- REGISTRATION COST ANTENUPTIAL CONTRACT - R1450

- FAQ - ANTENUPTIAL CONTRACTS

WHATSAPP -MESSAGE US! GET ANSWERS - GET INFORMATION

F.A.Q - Antenuptial Contracts

What is an Antenuptial Contract?

An antenuptial agreement, commonly known as a prenuptial agreement, is a legal contract couples enter before marriage. It serves as a crucial tool for defining each spouse's financial and property rights during their marriage and in the event of divorce or the death of one of the partners.

Key Points about Antenuptial Contracts:

Marriage Out of Community of Property:

An antenuptial contract allows couples to choose a marriage regime other than the default "in community of property". By default, when couples marry without an antenuptial contract, they are automatically married in community of property. This means that both spouses jointly own all assets and liabilities acquired before and during the marriage.

Opting for an antenuptial contract allows couples to keep their financial affairs separate. Each spouse retains ownership of their own assets and debts, and they do not share in each other's property.

Customisation and Flexibility:

Couples can tailor the terms of their antenuptial contract to suit their specific needs and circumstances. They can specify how assets, debts, and income will be managed during the marriage.

For example, if one spouse owns a business, they can protect it by excluding it from the joint estate. Similarly, if there are children from previous marriages, an antenuptial contract can ensure that their inheritance rights are safeguarded.

Freedom to Trade and Conduct Business:

An antenuptial contract provides the freedom for each spouse to engage in trade, business, and financial transactions independently. It allows them to manage their own assets, enter into contracts, and make investment decisions without the need for joint consent.

This is particularly important for entrepreneurs, professionals, and individuals with existing businesses or investment portfolios.

Legal Formalities:

An antenuptial contract must be drawn up by a qualified attorney and signed by both parties before the marriage ceremony.

It is then registered at the Deeds Office to make it legally binding.

Why Is an Antenuptial Agreement Important?

Asset Protection:

If one or both spouses have significant assets (such as property, investments, or businesses), an antenuptial contract ensures these assets remain separate and protected.

It prevents the automatic sharing of assets and liabilities that occurs in community of property marriages.

Debt Protection:

An antenuptial contract shields each spouse from the other's debts. If one spouse accumulates debt during the marriage, it does not automatically become the responsibility of the other.

Family Obligations:

An antenuptial contract can safeguard their inheritance rights if either spouse has children from a previous relationship. It ensures that their share of the estate is preserved, even if the marriage ends.

Clarity and Transparency:

Having a clear and legally binding agreement in place reduces misunderstandings and potential disputes during the marriage.

Both spouses know their rights and responsibilities, promoting transparency and trust.

In summary, an antenuptial contract provides couples with the freedom to define their financial arrangements according to their unique circumstances. It empowers them to protect their assets, manage their debts, and plan for the future, ensuring a more secure and harmonious marriage.

Louwrens Koen - Practicing Attorney, Notary and Conveyancer

Louwrens Koen Attorneys

When should we enter into an antenuptial contract?

Why should we consider an antenuptial contract?

- You are Marrying Someone with Significant Debt.

- You Wish to Protect Your Assets.

- You Want to Ensure Financial Security for Both Parties.

- You Want to Protect Your Business.

- You do not want to expose your spouse to your business risk.

How do we get started.

You and your future spouse will duly sign the Power of Attorney and Draft Antenuptial contract and return the original documents to us via courier (these courier costs will be for your account) or you can hand deliver the original documents to us.

Upon receipt of the original documentation, we will arrange for the execution thereof before a duly practising and admitted Notary Public who will also ensure that your Antenuptial Contract is registered in the Deeds office.

What matrimonial property regime is best for us?

Careful consideration should be given before deciding on the most suitable option. This article explains the diverse types of marriages available in South Africa and the formalities for concluding a legal marriage.

What types of marriages are there in South Africa?

The Matrimonial Property Act 88 of 1984

If after determining that your husband-to-be is domiciled in South Africa, then it is important for you to know that the Act that will be governing the assets of your estate going forward will be the Matrimonial Property Act 88 of 1984 (the Act). This Act will have a direct effect on your assets for the duration of your marriage, and at the possible termination, through either death or divorce. It is, therefore, important that you consider it carefully, and for this reason, I have briefly set out below the main points contained in the Act with which you need to acquaint yourself.

It is important to note that the South African matrimonial property regime was significantly amended in 1984, with the advent of the Matrimonial Property Act. Prior to this date, any marriage entered into without an ante-nuptial contract, resulted in the parties being married OUT of community of property.

This system was amended in 1984, with the intention of protecting the spouse who, during those times, gave up her career to stay at home and raise children. This amendment had the effect that Marriages entered without an ante-nuptial contract, resulted in the parties being married in community of property.

Options Pertaining to Marital Regimes in South Africa as According to the Act

If you are getting married to a South African as explained above, then you have 2 choices as to the marital regimes applicable to your marriage. They are:

1) A marriage in community of property; or

2) A marriage out of community of property.

If, however, you elect to be married out of community of property, which you must remember is not the default position, you require the execution of an ante-nuptial contract, in which case you have a further 2 choices:

1) Out of Community of Property with the application of the Accrual System; or

2) Out of Community of Property without the application of the Accrual System

How to decide which system is best for you?

One specific system is not necessarily the best for all couples. Which system is best will depend on the individual needs and circumstances of each couple. For this reason, the various regimes and their respective advantages and disadvantages will now be dealt with.

i) Marriage In Community of Property

How does it work?

In terms of this system, both spouses share equally in the assets and liabilities that either of them owns, owes, or acquires before or during the marriage.

Spouses will have equal power of administration, and both cannot practically act independently of the other, although there are certain exceptions.

Written consent of both is, however, required for certain important transactions such as those relating to a fixed property, suretyship and credit agreements, and informal consent of both is required for transactions such as the selling of goods of the joint household, such as furniture or jewellery. However, consent is not required for transactions relating to the trade, business, or profession of the spouses.

Advantages

This system rests on the sound principle namely that marriage is a partnership and as such can be conducive to a harmonious marital relationship. It also promotes both legal and economic equality of the spouses. During the marriage and on its dissolution both partners have entitled to a half share in the joint estate and each one has equal powers of administration.

Disadvantages

The biggest disadvantage of a marriage in a community of property is that the insolvency of one of the spouses affects the total communal property, and thus the solvency of the other spouse. Where a risk of insolvency exists, it is therefore not a desired system. Further, the system of equal powers could, in cases where the temperament of one or both marriage partners is not collaborative, lead to conflict in the marriage.

ii) Marriage Out of Community of Property Without The Accrual System

How does it work?

In this type of system, each spouse comes into the marriage with their own assets and debts. During the marriage, each spouse retains control of his or her own property, builds up his or her own estate and each is responsible for his or her own debts.

Advantages

Each spouse retains sole control of their own assets and liabilities. Consent of one spouse is not required by the other to allow each spouse to enter transactions, where each spouse is free to build up his or her own estate without the fear of it being attached by virtue of the other spouse's insolvency or being made liable to a division upon divorce.

Disadvantages

In this system, if one spouse gives up their career to care for a household or children, they or will be severely prejudiced by not benefitting from the estate that they helped to build by enabling the breadwinner to build up their wealth.

This system is therefore not recommended for couples where one spouse intends to give up work or where the couple’s earning capacities are hugely disparate.

iii) Marriage Out of Community of Property with the Accrual System

How Does it Work

This system was developed by the legislature especially to ensure that some protection is still offered to those parties who elect to marry out of the community of property, especially in those situations where, as referred to above, one of the parties remains at home, giving up a career to look after a household or children.

It works in much the same way as a marriage out of a community of property without accrual except that upon dissolution of the marriage, either by death or divorce, the estates of the parties will be divided differently in accordance with the respective assets and financial position of the parties.

The way in which this division takes place is that upon dissolution of the marriage, by death or divorce, the difference between the respective values of the assets of each spouse obtained during the marriage – the accrual – will be shared equally between the spouses. This means that the spouse whose estate has shown a larger growth will pay to the other spouse half of the difference in their respective accruals. The accrual is determined by calculating the difference in the net starting value and the net final value of the estate of each spouse with the exclusion of inheritances, legacies, and donations.

Advantages

Out of all the systems, it is accepted that the accrual system is a modern, equitable system and may be conducive to a harmonious marriage relationship. During the marriage, the competence of the spouses to deal with their property is not limited in any way, provided that the one does not or will not seriously prejudice the right of the other to share in the accrual. It also offers protection during the existence of the marriage against, for example, the insolvency of one of the spouses. Further, at the dissolution of the marriage, each spouse has a right to share in the growth of the estate, even if they did not financially contribute to it.

Disadvantages

A possible disadvantage, especially in the case of a wealthy spouse, might be that he or she feels that he or she is not quite free to deal with his or her property since the other could apply to the court for the immediate division of the accrual should the latter feel that the former, by entering into a specific transaction, might prejudice his or her right to share in the accrual. This may cause friction.

Another disadvantage of the accrual system is that spouses do not share in each other’s creditworthiness, which can the result that the non-working spouse may have little creditworthiness during the subsistence of the marriage if his or her estate is small.

What steps do you follow to let a particular system apply to your marriage?

Now that you have a better understanding of the types of systems that are available to you, it is important for you to know how to go about deciding how the regime you choose to apply is to be instituted. In this regard, it is important to remind the reader that should you marry without entering any form of ante-nuptial contract, you will automatically be married in community of property, and you will only be able to amend this by applying to the High Court.

If you enter an ante-nuptial contract but do not expressly exclude the accrual system, then this will automatically apply to your marriage. Should you wish to include the accrual system, but alter it in some way, you may do this by, for instance, including a provision that the eventual division of the accrual will not be on a 50/50 basis, but in accordance with another ratio.

It is important to note that you as spouses may include any provision that you wish to include in your ante-nuptial contract, if it is not contrary to the law.

Conclusion

To avoid any legal and practical difficulties arising from not selecting a matrimonial property regime from the outset, it is highly advisable that you contact a notary for more information on this topic. This should be done well in advance of getting married, to ensure that you have time to investigate and make suitable arrangements to comply with the legal requirements that apply to your intended marriage.

How long does it take to register an Antenuptial Contract?

Do we have to wait for registration of the antenuptial contract before we get married?

What is your cost to register an antenuptial contract?

I have questions?

How do we get our contract after registration?

What other services can you assist us with?

What matrimonial regime is best for us?

This article explains the different types of marriages available in South Africa, and the formalities for concluding a legal marriage.

What types of marriages are there in South Africa?

In South Africa a person can get married in terms of civil law or customary law, or in terms of a culture or religion, such as Hindu or Islamic law. This is provided that they follow the provisions of the Marriage Act when getting married and comply with the same requirements for a civil marriage during their religious or cultural ceremony. Even same-sex partners can get married by concluding a civil union. There are special requirements that the spouses of each type of marriage must comply with in order to render their marriage valid, and the requirements differ from one type of marriage to the next. It is very important to speak to your religious officer or marriage officer to ensure that your marriage will satisfy all of the legal requirements for such recognition.

Which laws apply to marriages concluded in South Africa?

When speaking of civil marriages and determining how you and your partner are going to get married, the first question that needs to be asked is which legal system applies to your marriage.

In terms of the common law in South Africa, the matrimonial property regime of a marriage is determined according to the law applicable in the husband’s country of domicile at the time of the marriage, as opposed to the wife’s country of domicile.

Domicile is sometimes a difficult concept to define, but the generally accepted legal definition is “the place which a person deems to be their permanent residence; or a place to which, even if he or she were temporarily absent, they intend to return.”

Thus, if you are a South African woman marrying a man from the United Kingdom who is temporarily in South Africa and intends on returning there in the near future, the default position is that the laws of the UK will apply to your marriage. If you are both South Africans residing in this country, then the legal systems of South Africa will apply to your marriage.

What is unclear, however, and yet to be decided by our courts, is what system will apply in a same-sex civil union. In this case how is it determined who the “husband” will be? This is a very serious issue which needs to be addressed on a Constitutional level.

The Matrimonial Property Act 88 of 1984

If after determining that your husband to be is domiciled in South Africa, then it is important for you to know that the Act that will be governing the assets of your estate going forward will be the Matrimonial Property Act 88 of 1984 (the Act). This Act will have a direct effect on your assets for the duration of your marriage, and at the possible termination, through either death or divorce. It is, therefore, important that you consider it carefully, and for this reason I have briefly set out below the main points contained in the Act with which you need to acquaint yourself.

It is important to note that the South African matrimonial property regime was significantly amended in 1984, with the advent of the Matrimonial Property Act. Prior to this date, any marriage entered into without an ante-nuptial contract, resulted in the parties being married OUT of community of property. This system was amended in 1984, with the intention of protecting the spouse who generally, during those times, gave up her career to stay at home and raise children. This amendment had the effect that Marriages entered into without an ante-nuptial contract, resulted in the parties being married IN community of property.

Options Pertaining to Marital Regimes in South Africa as According to the Act

If you are getting married to a South African as explained above, then you essentially have 2 choices as to the marital regimes applicable to your marriage. They are:

1) A marriage in community of property; or

2) A marriage out of community of property.

If, however, you elect to be married out of community of property, which you must remember is not the default position, you require the execution of an ante-nuptial contract, in which case you have a further 2 choices:

1) Out of Community of Property with the application of the Accrual System; or

2) Out of Community of Property without the application of the Accrual System

How to decide which system is best for you

One specific system is not necessarily the best for all couples. Which system is best will depend on the individual needs and circumstances of each couple. For this reason, the various regimes and their respective advantages and disadvantages will now be dealt with.

i) Marriage In Community of Property

How does it work?

In terms of this system, both spouses share equally in the assets and liabilities that either of them own, owe or acquire before or during the marriage.

Spouses will have equal power of administration and both can act independently of the other, although there are certain exceptions. Written consent of both is, however, required for certain important transactions such as those relating to fixed property, suretyship’s and credit agreements, and informal consent of both is required for transactions such as the selling of goods of the joint household, such as furniture or jewellery. However, consent is not required for transactions relating to the trade, business or profession of the spouses.

Advantages

This system rests on the sound principle namely that marriage is a partnership and as such can be conducive to a harmonious marital relationship. It also promotes both legal and economic equality of the spouses. During the marriage and on its dissolution both partners are entitled to a half share in the joint estate and each one has equal powers of administration.

Disadvantages

The biggest disadvantage of a marriage in community of property is that insolvency of one of the spouses affects the total communal property, and thus the solvency of the other spouse. Where a risk of insolvency exists, it is therefore not a desired system. Further, the system of equal powers could, in cases where the temperament of one or both marriage partners is not collaborative, lead to conflict in the marriage.

ii) Marriage Out of Community of Property Without The Accrual System

How does it work?

In this type of system, each spouse comes into the marriage with their own assets and debts. During the marriage each spouse retains control of his or her own property, builds up his or her own estate and each is responsible for his or her own debts.

Advantages

Each spouse retains sole control for their own assets and liabilities. Consent of one spouse is not required by the other so as to allow each spouse to enter into transactions, where each spouse is free to build up his or her own estate without the fear of it being attached by virtue of the other spouses insolvency, or being made liable to a possible division upon divorce.

Disadvantages

In this system, if one spouse gives up their career to care for a the household or children, they will be severely prejudiced by not benifitting from the estate that they essentially helped to build by enabling the bread winner to build up their wealth.

This system is therefore not recommended for couples where one spouse intends giving up work or where the couple’s earning capacities are hugely disparate.

iii) Marriage Out of Community of Property With the Accrual System

How Does it Work

This system was developed by the legislature especially to ensure that some protection is still offered to those parties who elect to marry out of community of property, especially in those situations where, as referred to above, one of the parties remains at home, giving up a career to look after a household or children.

It works in much the same way as a marriage out of community of property without accrual except that upon dissolution of the marriage, either by death or divorce, the estates of the parties will be divided differently in accordance with the respective assets and financial position of the parties.

The way in which this division takes place is that upon dissolution of the marriage, by death or divorce, the difference between the respective values of the assets of each spouse obtained during the marriage – the accrual – will be shared equally between the spouses. This means that the spouse whose estate has shown a larger growth will pay to the other spouse half of the difference in their respective accruals. The accrual is determined by calculating the difference in the net starting value and the net final value of the estate of each spouse with the exclusion of inheritances, legacies and donations.

Advantages

Out of all the systems, it is generally accepted that the accrual system is a modern, equitable system and may be conducive to a harmonious marriage relationship. During the marriage the competence of the spouses to deal with their property is not limited in any way, provided that the one does not or will not seriously prejudice the right of the other to share in the accrual. It also offers protection during the existence of the marriage against, for example, insolvency of one of the spouses. Further, at the dissolution of the marriage each spouse has a right to share in the growth of the estate, even if they did not financially contribute to it.

Disadvantages

A possible disadvantage, especially in the case of a wealthy spouse, might be that he or she feels that he or she is not quite free to deal with his or her property since the other could apply to court for the immediate division of the accrual should the latter feel that the former, by entering into a specific transaction, might prejudice his or her right to share in the accrual. This may cause friction.

Another disadvantage of the accrual system is that spouses do not share in each other’s credit worthiness, which can have the result that the non-working spouse may have little credit worthiness during the subsistence of the marriage if his or her estate is small.

What steps do you follow to let a particular system apply to your marriage?

Now that you have a better understanding of the types of systems that are available to you, it is important for you to know how to go about deciding how the regime you choose to apply is to be instituted. In this regard, it is important to remind the reader that should you marry without entering into any form of ante-nuptial contract, you will automatically be married in community of property and you will only be able to amend this by applying to the High Court.

If you enter into an ante-nuptial contract but do not expressly exclude the accrual system, then this will automatically apply to your marriage. Should you wish to include the accrual system, but alter it in some way, you may do this by, for instance, including a provision that the eventual division of the accrual will not be on a 50/50 basis, but in accordance with another ratio.

It is important to note that you as spouses may include any provision that you wish to include in your ante-nuptial contract, provided that it is not contrary to the law.

Conclusion

In order to avoid any legal and practical difficulties arising from not selecting a matrimonial property regime from the outset, it is highly advisable that you contact a marriage officer, attorney or notary for more information on this topic. This should be done well in advance of getting married, to ensure that you have time to investigate and make suitable arrangements to comply with the legal requirements that apply to your intended marriage.

How do I get to your offices?

We are located within the Northern Pavilion of Loftus Ver2veld Stadium.

Louwrens Koen Attorneys

Office 4, Second Floor, Northern Pavilion, Loftus Versveld Stadium,

416 Kirkness Street, Pretoria

Tel:0870010733 E-mail admin@louwrenskoen.co.za

Or search for Louwrens Koen Attorneys and Google Maps.

Why should we use Louwrens Koen Attorneys to register our Antenuptial contract?

How do I get a copy of my invoice? When do we pay?

OUR TEAM IS HERE TO ANSWER YOUR ANTENUPTIAL CONTRACT QUESTIONS

CONTACT US TODAY AND WE WILL REPLY WITHIN HOURS Louwrens Koen Attorneys Tel: 0870010733 admin@louwrenskoen.co.za

Donations between spouses in antenuptial contracts

The prohibition against donations between spouses was repealed by the Matrimonial Property Act. Donations between spouses do not form part of the accrual, unless the parties agree otherwise in the contract Donations set out in the antenuptial can serve as proof on the insolvency of one of the spouses that the property in question belongs to the other solvent spouse.

This is of particular advantage to the spouses when the goods in question are attempted to be attached. Where the accrual systems is excluded in terms of the contract, the “breadwinner” spouse can out of consideration of fairness and to acknowledge the other spouse's contribution to the marriage, make donations in favor of that spouse. No donation tax is payable in respect of the value of property which is donated to the spouse of the donor under a duly registered antenuptial/postnuptial contract.

No estate duty is payable on the value of property donated to or for the benefit of the spouse of the donor under a duly registered antenuptial/postnuptial contract.

Clauses that may not be entered in a antenuptial contract

Clauses that are regarded as contra bonis mores and which may not be included in the antenuptial contract

The parties are free to include any provision in the antenuptial contract, as long as it is not against nature, reason, morality, public policy or prohibited by law. Clauses of this nature will be null and void.

Clauses that are regarded as contra bonis mores and which may not be included in the antenuptial contract:

1. An undertaking by a spouse to change religion.

2. A clause stating that marital disputes must be referred to arbitration.

3. A clause recreating the husband’s marital power.

4. A clause stating that the parties will not live together as man and wife after the marriage.

5. A clause permitting the parties to commit adultery.

6. A clause where one of the parties undertakes to resign after marriage.

Herewith are some common clauses that may be entered into an antenuptial contract.

- Exclude Community of Property

- Profit and Loss

- Include or exclude the Accrual system

- Changing Percentage of Accrual

- Donations between Spouses

- Insurance policies

- Exclusion of particular assets

- Mutual will (Pactum Successorium)

- Creation of a Trust

Getting Married? - Handy Hints to get the DIFFICULT TOPIC OF AN ANTENUPTIAL Contract going

Discussing the necessity of an antenuptial contract may be a difficult discussion to have with your intended spouse. Because your choice will have significant legal and financial implications it is essential for the parties to explore their options before getting married.

It is also evident that there are misconceptions and antagonism about and against antenuptial contracts. As one lady eloquently stated, "We love each other! We don't need it". It was, however, very telling when this young lady's mother came back later to collect a brochure.

It is also saddening for the writer when he consults with couples married in community of property to see the devastation caused when they lose everything due to not taking the time to plan and mitigate their risks.

We understand that to the bride and groom, marriage is a loving contract between two people, as it should be, who want to spend the rest of their lives together. In the eyes of the Law and corporate business, marriage is also a contract between two people not about love, the matrimonial property regime they choose before getting married regulates a variety of economic rights, freedom to trade, exposure and obligations.

Should you thus not elect yourself, the Law will decide on your behalf. If you care about your spouse, you, therefore, owe it to yourself and your spouse to take the time to explore your options. Agreeing beforehand on these matters will put your marriage on a sounder footing.

It's hard to talk about marriage as if it were "business," but when it comes to creating a prenuptial agreement, that's precisely the approach you should take. A prenuptial agreement isn't a plan to leave or evidence of a lack of faith in the relationship. It merely is legal protection against the future risk you may be exposed to.

Start the conversation well before getting married

Don't wait until a week before your wedding to discuss a prenuptial agreement with your intended. Explore the topic early in a relationship, if possible, before you become engaged.

Don't assume you are on the same page with your intended spouse.

People have all kinds of notions about antenuptial contracts from their own experiences and subjective view. Don't assume that you and your spouse-to-be are on the same page with this topic; ask.

Use your head. Not your heart.

It's tough to talk about your loving, committed relationship as if it were a business arrangement. If you and your intended can agree to be logical (rather than emotional) about preparing an antenuptial contract, you'll find it much more manageable.

Always consult your Attorney.

If your spouse-to-be is hesitant, suggest that they consult a legal professional to explore the benefits. You may find iso consult with a legal professional to understand the different k might be covered in an antenuptial contract. The more informed you are, the easier it will be to explain things to your intended.

Whatever your decision may be. Please take the time to consider your options. Also, could you consider changing or amending your will and estate planning when getting married?

Louwrens Koen Attorneys have assisted thousands of couples with choosing the appropriate antenuptial contract. Please do not hesitate to contact us.

Louwrens Koen - Practicing Attorney, Conveyancer and Notary Public.

Contact Us

Clauses thatTHAT MAY not be included in the antenuptial contract

1. An agreement that one spouse will adopt or convert to the religion/faith of the other.

2. An agreement that marital disputes will be referred to arbitration.

3. A clause that re-establishes or maintains the husband’s marital power.

4. A clause that states the parties will not live together after marriage.

5. A clause that permits either party to commit adultery.

6. A clause that requires the wife to stop working and become a housewife from the birth of their first child.

7. A clause that prevents either spouse from binding the other for household expenses.

8. A clause that denies either spouse the right to ask for a share of the other’s estate in the event of divorce.

AMENDMENTS AND RECTIFICATIONS TO ANTENUPTIAL AGREEMENTS

Amendments of antenuptial contracts prior and after the date marriage

However, if both of parties provide valid reasons, the High Court can grant an order to amend or rectify the contract to reflect the true intentions of the parties. All other parties must also agree to the rectification. This will come at a cost. Article 4(1)(b) of the Deeds Registries Act also allows for an amendment to fix errors in the antenuptial contract. For example, an error in the name of a party, date of birth, identification number, property description, and life insurance policy can be rectified in this manner.

Amendment to rectify an error

An amendment to rectify an error in the antenuptial contract can be done by means of an application to the registrar of deeds in terms of Article 4(1)(b) of the Deeds Registries act

Examples of errors that can be rectified in this manner are:

- An error in the name of a party;

- An error in the date of birth of a party;

- An error in the identity number of a party;

- An error in the property description in a donation clause; and

- An error in the number of the life insurance policy to be ceded.

consequances of marriage that cannot bealtered by an antenuptial contract

• The obligation to have a joint household and to live together as man and wife.

• The obligation to treat each other with decency, fairness and respect.

• The obligation to allow each other the privileges of marriage.

• The obligation to be loyal and committed to each other.

• That both parties will attain and retain full legal capacity (in the case that one of or both parties are minors).

wHAT ARE THE DEFINITION AND PURPOSE OF AN ANTENUPTIAL CONTRACT?

The purpose of an antenuptial contract is to exclude the community of property and profit and loss as well as to include or exclude the accrual system from the marriage.

Formalities regarding the registration of an Antenuptial Contract

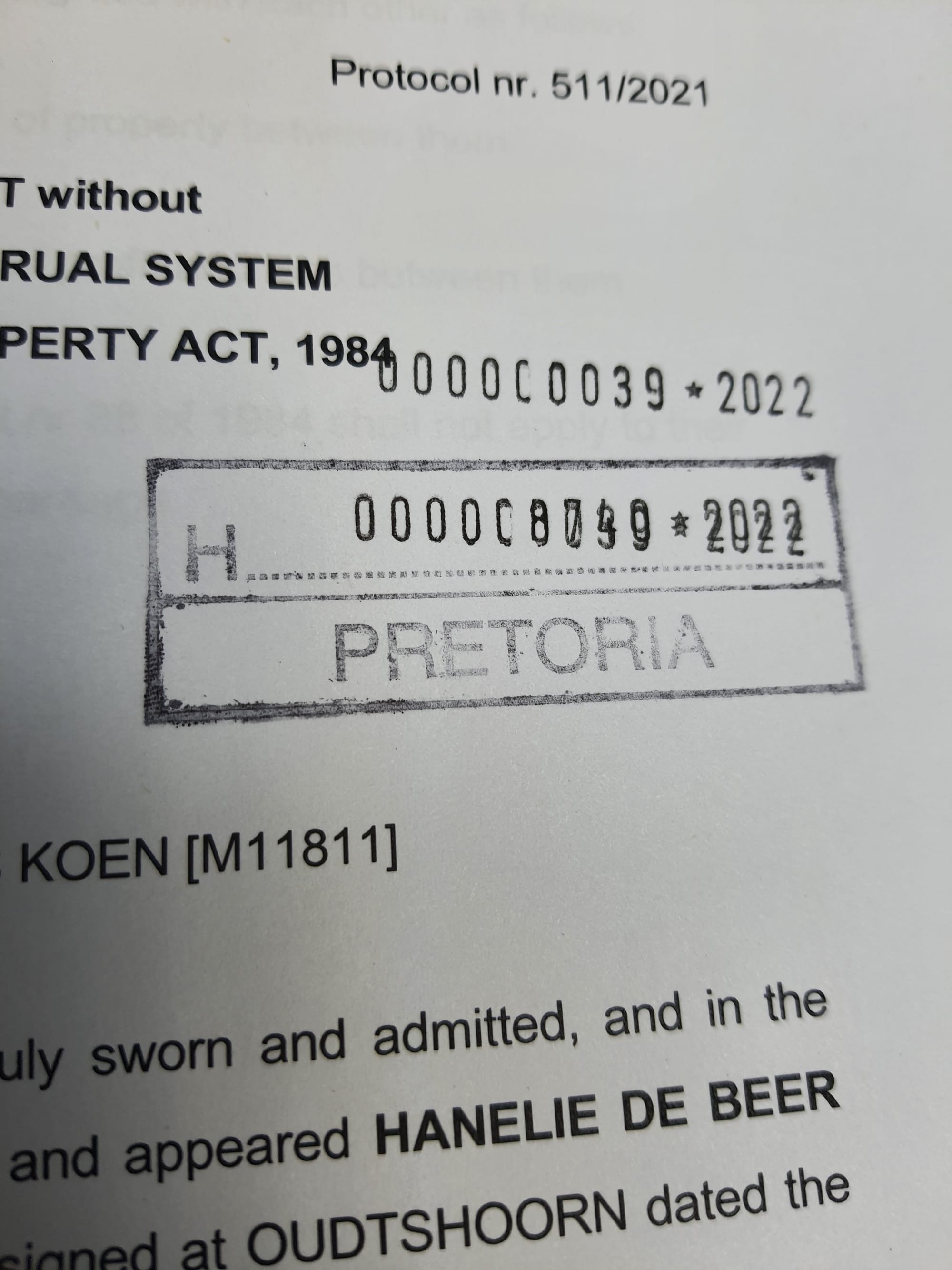

The two intended spouses must sign the contract before two competent witnesses of at least 14 years of age who can give evidence in court. The place of execution must be stated in the contract, and if the parties sign on different dates, the latest date will be regarded as the date of the contract. If a third person is included in the contract, they must also sign it. Antenuptial contracts executed in South Africa must be registered in the office of the Registrar of Deeds within three months of the date of execution or within such an extended period as the court may allow if the application is made. Contracts executed outside South Africa must be attested by a notary and legalised and registered in a deed's registry within six months of the date of execution.

If a contract is not registered within the stipulated time, it will have no force or effect against third parties but will be valid between them. Registration of an antenuptial contract in any of the offices of the Registrar of Deeds is effective throughout South Africa.

Formalities to enter into a valid marriage

The parties must have the appropriate capacity to enter into a valid marriage. For marriages under the Marriage Act 1961, minors between the age of puberty and the age of majority must have the consent of both parents or a guardian. If the minor has only one parent living, only that parent's consent is required. Where the minor has a guardian, the guardian's consent is needed. If the minor has no parent or guardian, permission must be obtained from the Commissioner of Child Welfare. Additional consent is required from the Minister of Home Affairs if the male minor is under the age of 18 and the female is under the age of 15. For marriages and civil partnerships under the Civil Union Act, the age of consent is 18.

In terms of common law, insane persons cannot enter into a valid marriage. This is due to their lack of understanding of the nature of the juristic act and the obligations that marriage creates. Where a person marries whilst they are already validly married to someone else, the second marriage will be bigamous and therefore void. Bigamy is a criminal offence. Both parties must have the intention to conclude a marriage as understood by the law.

This is evidenced by their declarations to the marriage officer during the marriage ceremony. Consensus will be excluded by a material mistake as to the spouse's identity or the nature of the juristic act, duress or undue influence, or prenuptial stuprum. The law also prohibits marriage between certain blood relations (relationship of consanguinity) and certain persons related through marriage (relationship of affinity). Marriages within these prohibited degrees of relationship are not valid and are in fact, void.

The formal requirements for entering a valid marriage are contained in the Marriage Act (25 of 1961) and the Civil Union Act (17 of 2006). A duly appointed marriage officer must solemnise the marriage, each party must produce an identity document or an affidavit in the prescribed form, and a minor must produce written consent of their parent(s) or guardian. The marriage officer must solemnise the marriage according to the prescribed formula in the presence of the two parties to the marriage and in the presence of two witnesses. All marriages must be registered. If the prescribed formalities are not complied with, the marriage is void marriage.

PACTUM SUCCESSORUM

Succession clauses in antenuptial contracts explained.

Succession clauses in an antenuptial contract are an exception to the rule that agreements relating to inheritance are unenforceable. The parties may make provision for the succession of the survivor of them to the estate (or part thereof) of the first dying spouse. Such a provision cannot be revoked unilaterally in a subsequent will without the consent of the benefiting party. Examples "The parties declare that on the death of either of them, the survivor shall be entitled to the whole estate of the first dying."

"The parties declare that upon the death of the first death of them, all assets belonging to such a party shall pass to the surviving spouse." The parties may also insert other testamentary provisions in the antenuptial contract, for example, revocation of previous wills, the appointment of executors and heirs, the establishment of a mortis causa trust etc. See the model answer to Notarial Practice Examination - October 2002, Question 3, for an example of an antenuptial contract incorporating other testamentary provisions. It is also possible for a third person to bequeath his or her property to one or both of the spouses in the antenuptial contract. Just remember that the third person must then be joined as a party to the contract, and he or she must also sign the contract in the presence of a notary.

The third-party cannot revoke such a bequest without the consent of the benefiting spouse(s). Succession clauses in an antenuptial contract are an exception to the general rule that agreements regarding inheritance are not legally enforceable. Through such a clause, the spouses can agree that the survivor of them will be entitled to the estate, or part thereof, of the first dying spouse.

This cannot be changed unilaterally by either spouse in a subsequent will without the consent of the other. Furthermore, the antenuptial contract can also include other testamentary provisions such as the revocation of previous wills, the appointment of executors and heirs, the establishment of a mortis causa trust, etc.

It is also possible for a third party to bequeath their property to one or both spouses in the antenuptial contract. In such a case, the third person must be a party to the contract and sign the contract in the presence of a notary. The third-party cannot then revoke the bequest without the consent of the benefiting spouse(s).

The section 6(1) Statement

Declaring nett commencement value in a separate document not registered in the office of the Registrar of Deeds

Section 6(1) of Act 88 of 1984 provides that parties may declare the net commencement values of their respective estates within six months of the commencement of the marriage. If the parties did not state the net commencement values of their respective estates in the antenuptial contract, they may execute a statement in accordance with this section. The statement is not required to be lodged and registered at the deeds office and is instead held by the notary in their protocol. High nett-worth individuals usually do not want to declare their nett asset worth in a public document.

Unenforceable Clauses in a Marriage Contract

According to Louwrens Koen Attorneys, clauses in a marriage contract (ANC) may be deemed unenforceable if they are against public policy, against the good morals of the public, unreasonable, prohibited by law, or aim to take over the powers of the court. These clauses will be null and void.

Examples of unreasonable clauses in a marriage contract include:

- Prohibiting a spouse from working

- Forcing a spouse to live in a specific area

- Requiring marital disputes to be resolved through arbitration

- Obligating a spouse to adopt the religion of the other spouse

- Stating that the spouses will not live together after the marriage

- Preventing either spouse from seeking a forfeiture or share in the other's estate after a divorce.

Clauses against public policy include:

- Enforcing a change in religion, gender, or race

- Prohibiting association

- Allowing or forcing a spouse to commit a crime.

Clause to deter infidelity: A clause in an ANC that aims to prevent infidelity by a spouse is enforceable if it seeks to preserve the marriage by discouraging extramarital affairs. For example, if a clause states that the husband will pay the wife a fixed property or cash amount if it is proven that he caused a future divorce through an extramarital affair, the court may enforce this clause.

Costs - R1550

New Slogan

Free 20 min Consultation - Antenuptial Contract

- When you have gone through all the provided articles and frequently asked questions and still have questions. Or you have unique circumstances you wish to discuss in person with an specialist attorney. Sometimes the parties prefer to sign the agreement before the Notary Public in person. Only available if you have already registered and paid for the registration of an antenuptial contract.

Antenuptial Contract - Register

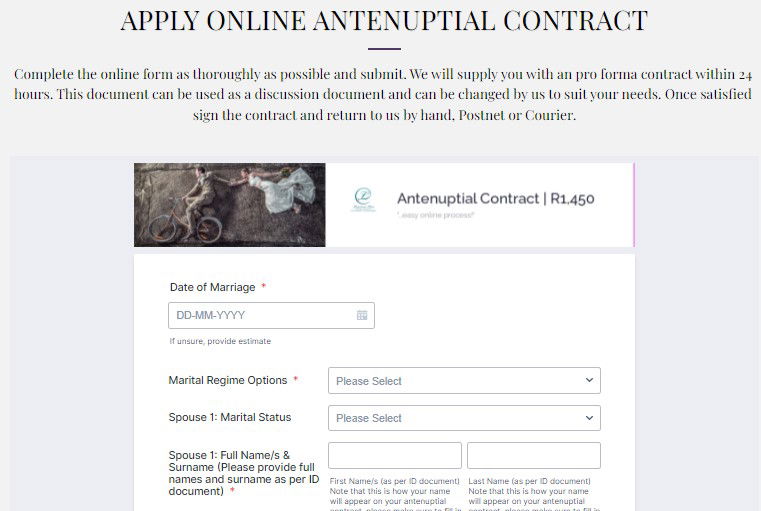

MOST POPULAR- Online Application Form Antenuptial Contract - Our Process - Get Started

- Complete the online form as thoroughly as possible and submit. We will supply you with an pro forma contract within 24 hours. This document can be used as a discussion document and can be changed by us to suit your needs. Once satisfied sign the contract and return to us by hand, Postnet or Courier. We will supply detailed instructions. Contact us anytime if you have any questions.

- Congratulations on your pending nuptials. Start your journey.

Antenuptial Contracts - Resources

Antenuptial Contract Brochure

Antenuptial Contracts Explained

Matrimonial Property Act 88 of 1984

Down Matrimonial Property Act PDF

Recognition of Customary Marriages Act

To makeprovision for the recognition of customary marriages; to specify the requirements for a valid customary marriage; to regulate the registration of customary marriages; to provide for the equal status and capacity of spouses in customary marriages; to regulate the proprietary consequences of customary marriages and the capacity of spouses of such marriages; to regulate the dissolution of customary marriages; to provide for the making of regulations; to repeal certain provisions of certain laws; and to provide for matters connected therewith.

Online Application - Get Started

Complete the online form as thoroughly as possible and submit. We will supply you with an pro forma antenuptial contract within 24 hours. This document can be used as a discussion document and can be changed by us to suit your needs if necessary. Once satisfied sign the contract and return to us by hand, POSTNET or Courier. We will supply detailed instructions.

Testimonials - Louwrens Koen Attorneys

See what our clients say about us.

About Our Antenuptial Contract Registration Service

12 Years running - Thousands of couples assisted using our online application process.

Using our efficient online application form we have assisted thousands of couples. We pride ourselves in being approachable. Do not hesitate to contact us with your questions or schedule a free consultation. Louwrens Koen Attorneys

Contact

- Louwrens Koen Attorneys 417 Kirkness Street, Sunnyside, Pretoria, South Africa

- +27870010733

- admin@louwrenskoen.co.za

- Mon - Thurs: 8 am - 16h30 pm Fri: 8 am - 16h00 pm Sat - Sun: Closed

Louwrens Koen Attorneys have assisted thousands of couples to register an antenuptial contract. We pride ourselves in being very approachable. As this will affect your legal status and is therefore an very important matter do not hesitate to contact with any questions you might have.

F.A.Q - Antenuptial Contracts

What is an Antenuptial Contract?

What is the difference between Antenuptial and prenuptial agreement?

What is an antenuptial contract with accrual?

Can an antenuptial contract be signed after marriage?

What is the purpose of an antenuptial contract?

What is excluded from accrual?

These are assets owned by either spouse, or even by the spouses jointly, that they want to ignore when calculating accrual. By excluding an asset, you prevent your spouse from obtaining any benefit from the growth on the value of that asset during the marriage.

How much does an antenuptial contract cost?

What do you need for an antenuptial contract?

The contract must be entered into/ signed before the marriage, The said contract must further be executed in front of two competent witnesses and attested by a notary before the marriage, Once executed the contract must be registered in the Deeds Office within 3 months of executing the contract.

How does antenuptial contract work?

How are accrual claims calculated?

How to calculate the accrual?

- DETERMINE THE VALUE OF THE ASSETS: Draft a list of all the assets. ...

- DEDUCT THE FOLLOWING FROM THE TOTAL VALUE OF THE ASSETS: The commencement value as stated in the antenuptial contract (adjusted to be in line with the weighted average of the Consumer Price Index), ...

- THE RESULT = “The Accrual”

Is an oral antenuptial contract valid?

Where must an antenuptial contract be registered?

Who must execute a prenuptial contract?

Pros and Cons of Marrying Out Of Community Of Property With Accrual

- The spouses share the increase in their assets accumulated during the marriage and the economically weaker spouse will benefit.

- The spouses do not share their assets acquired before their marriage (but only if excluded in the ANC or included in the commencement values of the parties’ estates). The accrual system appeals to people who are already wealthy at the time of marriage.

- During the course of the marriage, each spouse manages his/her estate at will. There is no complex joint or equal administration.

- The spouses are not liable for each other’s debts. All that they share is their net assets. Thus, if one spouse becomes insolvent, the other spouse is protected against creditors.

- The economically stronger spouse has to share the profits that he/she made during the marriage.

- One has to enter into an ANC in order for the accrual system to apply.

- The calculation of accrual at the end of the marriage can be a bit complex.

Pros and Cons of Marrying Out Of Community Of Property Without Accrual

- Each party will keep their individual assets and liabilities separate and can handle it however he/she likes.

- Spouses are not liable for each other’s debts, thus if one spouse becomes insolvent creditors cannot make a claim against the solvent spouse with regards to their assets.

- The financially and/or economically stronger spouse is not legally obligated to share his/her assets with the financially and/or economically weaker spouse. This is subject to judicial discretion and forfeiture of benefits.

- The economically and/or financially weaker spouse does not get to share in the estate of the economically and/or financially stronger spouse even if the other party indirectly contributed.

- An ANC has to be entered into prior to marriage which incurred additional fees.

What is a Civil Union Marriage?

A “civil union” is a “voluntary union of two persons who are both 18 years of age or older, which is solemnised and registered by way of either a marriage or a civil partnership, in accordance with the Act, while it lasts, to the exclusion of all.

The same practices and procedures applicable to the registration of antenuptial contracts of persons married in terms of the Marriage Act 25 of 1961 apply to the registration of antenuptial contracts of persons joined in a civil union. The legal consequences of a marriage contemplated in the Marriage Act and the provisions of the Matrimonial Property Act 88 of 1984 apply to a civil union in exactly the same manner as it is applicable to persons married in terms of the Marriage Act.

What are the proprietary consequences of a customary marriage?

Customary marriages entered into before commencement of the Act remains subject to customary law. The spouses may nevertheless apply to the court for leave to change the matrimonial property system applicable to their marriage -

Does a ninor need permission to marry

If an intended spouse is still a minor, he/she must be assisted by one of his/her parents or by his legal guardian when executing the antenuptial contract Although only the consent of one of the parents or the legal guardian is required to the entering into of the antenuptial contract, both parents must consent to the contracting of the marriage.

Take note that the minor himself must sign the contract. The parent or guardian may not sign the contract on behalf of the minor. The parent or guardian will simply signify his/her assistance by co-signing the contract together with the minor.

Both parents must assist the minor if the antenuptial contract makes provision for any alienation of immovable property or a right to immovable thereto belonging to the minor. If the parent/s or the legal guardian of the minor refuses to consent to the minor entering into the antenuptial contract, the High Court as upper guardian may on application grant the necessary consent

A marriage entered into by a minor without the necessary consent is not void, but may be dissolved by the High Court on application by the parents or legal guardian of the minor. The application must be brought before the minor attains majority or within 6 weeks after the date on which the guardian became aware of the marriage.

How is Accrual Calculated?

The value of each spouse’s estate at commencement of the marriage must either be disclosed in the antenuptial contract or in a separate statement. If no value is recorded, the nett commencement value will be presumed to be nil.

On dissolution of the marriage each spouse’s estate will be valued again in order to calculate the growth/accrual of each estate. The commencement values are adjusted to make provision for inflation. The following assets are however left out of account in calculation of the accrual, unless the antenuptial contract provides to the contrary:

- Damages received for non-patrimonial loss ;

- Inheritances, legacies and donations received from third parties Section

- Assets especially excluded from the accrual in the antenuptial contract -

- Donations between the spouses -

How is the accrual system included?

How is the Accrual System Excluded in an antenuptial contract?

Example

“The said intended marriage will not be subject to the provisions of Chapter I of the Matrimonial Property Act 88 of 1984 and the accrual system is hereby expressly excluded.”

What is a Notary Public?

What does a Notary do?

Part of a Notary's duty is to screen the individuals who sign important documents for their true identity, their awareness of the contents of the document or transaction, and their willingness to sign without coercion or intimidation. Some situations require a Notary to put the individual under oath, declaration under penalty of perjury that the information contained in a document is true and correct.

A Notary Public has to have impartiality as a foundational value. They need to be duty-bound and thus cannot act in situations with personal interest. The public trusts that the Notary's screening tasks are corruption-and self-interest free. Impartiality also assures that a Notary never refuses to serve a person due to their religion, race, nationality, politics, sexual orientation, or status as a non-customer.

By law, the following documents need to be drawn up by a Notary:

- Antenuptial Contracts

- Long-term Leases

- Servitudes (personal and praedial)

- Cession of Rights in Sectional Title Schemes

- Notarial Bonds

- Marriage certificates

- Birth certificates

- Death certificates

- Single status certificates

- Divorce certificates

- Police clearance certificates

- Powers of attorney

- Copies of IDs or passports

- Educational documents

Why you should consider an Antenuptial Contract before getting married?

Does a husband have marital power over his wife in terms of South African law?

Explain Accrual as set out in the Matrimonial Property Act

It operates by separating the assets of each spouse during the marriage and only sharing any gains made during the marriage on dissolution. Assets owned by either spouse prior to the marriage are not subject to this system. To calculate the accrual, the value of each spouse's estate at the commencement of the marriage must be disclosed in the antenuptial contract or a separate statement. If no value is stated, it is presumed to be zero. Upon dissolution of the marriage, each spouse's estate is valued again, adjusted to make provision for inflation, and the gain (accrual) is calculated.

The accrual system applies automatically to marriages out of community of property, unless it is expressly excluded in the antenuptial contract. If the parties do not wish to be subject to the system, they must insert a clause in their contract stating so. It is possible to modify the system in a number of ways.

For example, the parties may make the system applicable only after a certain time period or after a child has been born or make it inoperative if either party's estate is insolvent. They may also opt to have inheritances, legacies, donations, and donations between spouses taken into account for calculation of the accrual.

They may even agree to share the accrual in a different percentage than the prescribed 50/50. Within six months of the marriage, the parties may declare the net value of their respective estates either in the contract or in a separate statement certified by a notary and kept in his protocol. If the parties do not wish their values to be public, they must make use of the separate statement.

OUR TEAM WILL ANSWER YOUR ANTE NUPTIAL CONTRACT QUESTIONS

CONTACT US TODAY AND WE WILL GET RIGHT BACK TO YOU

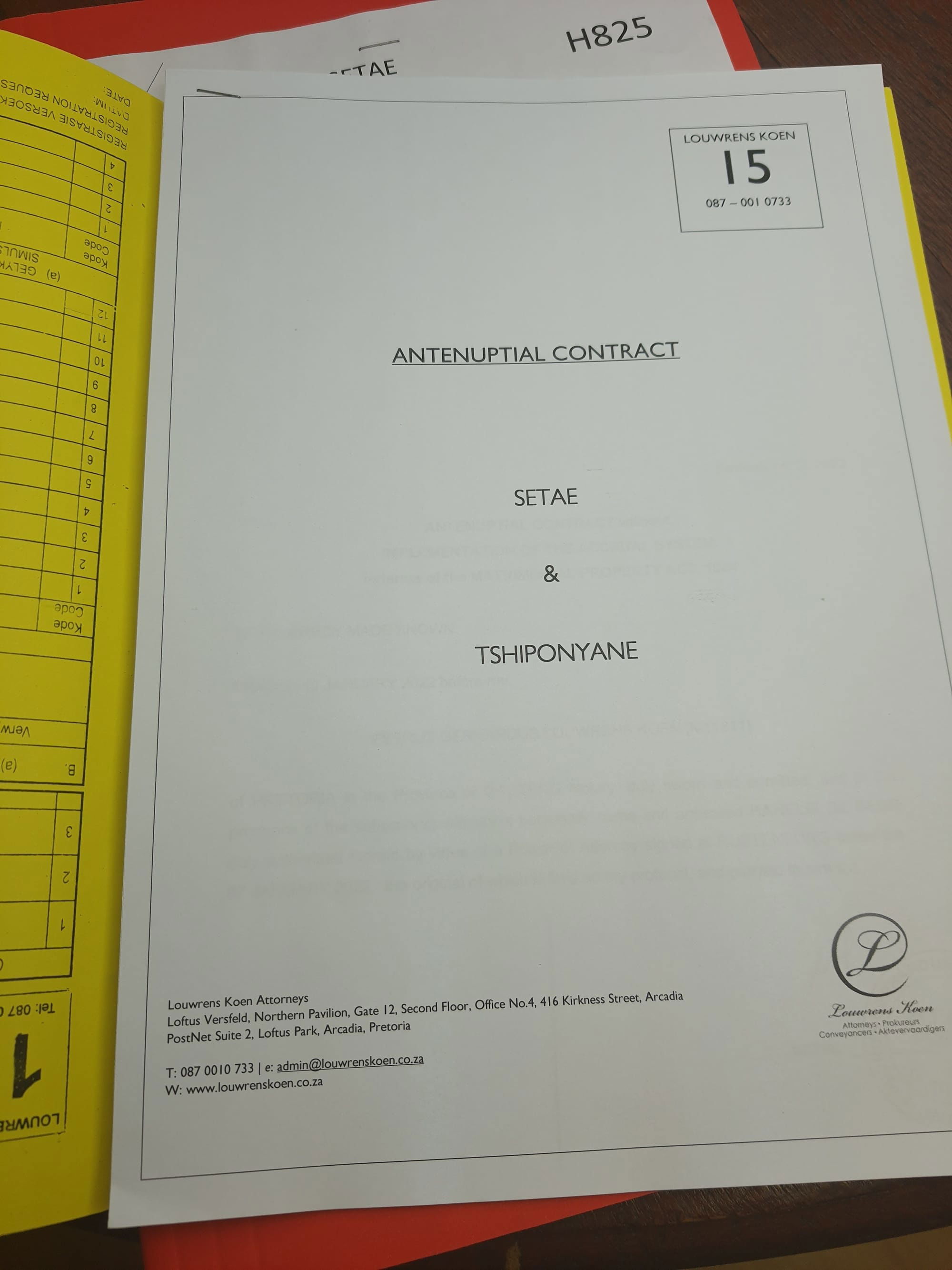

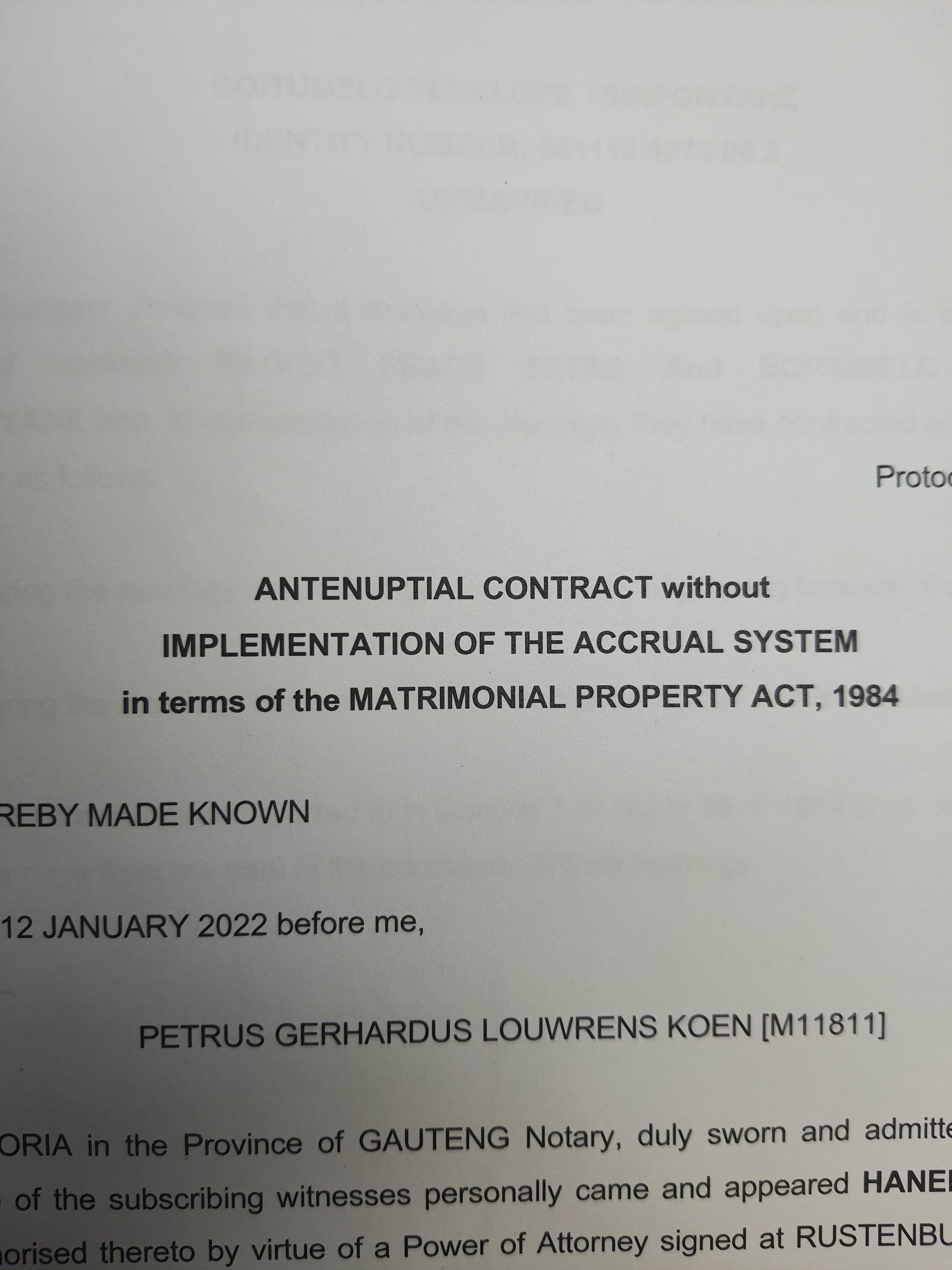

Gallery IMAGES Antenuptial Contracts

Images of Antenuptial Contracts and Louwrens Koen Attorneys Offices

OUR TEAM IS HERE TO ANSWER YOUR ANTENUPTIAL CONTRACT QUESTIONS

CONTACT US TODAY AND WE WILL REPLY WITHIN HOURS Louwrens Koen Attorneys Tel: 0870010733 admin@louwrenskoen.co.za

Podcasts - Antenuptial Contracts

CAPE TALK PODCAST OF ANTENUPTIAL CONTRACTS INTERVIEW WITH LOUWRENS KOEN

what is a notary public?

What does a Notary do?

Part of a Notary's duty is to screen the individuals who sign important documents for their true identity, their awareness of the contents of the document or transaction, and their willingness to sign without coercion or intimidation. Some situations require a Notary to put the individual under oath, declaration under penalty of perjury that the information contained in a document is true and correct.

A Notary Public has to have impartiality as a foundational value. They need to be duty-bound and thus cannot act in situations with personal interest. The public trusts that the Notary's screening tasks are corruption-and self-interest free. Impartiality also assures that a Notary never refuses to serve a person due to their religion, race, nationality, politics, sexual orientation, or status as a non-customer.

By law, the following documents need to be drawn up by a Notary:

- Antenuptial Contracts

- Long-term Leases

- Servitudes (personal and praedial)

- Cession of Rights in Sectional Title Schemes

- Notarial Bonds

- Marriage certificates

- Birth certificates

- Death certificates

- Single status certificates (Letter of No Impediment)

- Divorce certificates

- Police clearance certificates

- Powers of attorney

- Copies of IDs or passports

- Educational documents

For further information please visit our informative notary related websites:

Apostilles.Africa - Document Legalisation & Notary Public Services

Notary.Africa - Notary Public Services South Africa

PostnuptialContracts. co. za - Register Postnuptial Contract after marriage.

Cohabitation Contracts .co.za - Registration of Cohabitation / Life Partnership Agreements

Antenuptial Contracts and Their Impact on Joint Businesses in Marriage

Antenuptial contracts (ANCs) allow couples to marry out of community of property. This is a popular option for those who want to protect their assets and finances before and during their marriage. With an ANC, each spouse retains their right to contract with third parties without the other's consent and is protected from the creditors of the other spouse.

When marrying out of community of property, there are two options to consider regarding the ANC: with or without accrual. Marrying without accrual means that each spouse keeps their own property and liabilities acquired prior to and during the marriage. With accrual, each spouse is entitled to a fair share of the estate in case of a divorce. The default option is marrying with accrual, which is automatically included if the accrual system is not excluded in the ANC.

A recent court case (RD v TD 2014 (4) SA 200 (GP)) highlights potential legal loopholes for couples who choose to marry with an ANC without accrual and later engage in a joint business venture. The court ruled that these spouses should be treated as business partners and the net benefits from the partnership would be divided between them. It is important for couples to have these difficult discussions and understand the consequences of their marriage regime before entering into it, to protect themselves and their future spouse in the event of a divorce or death.

For expert advice on matrimonial systems and related topics, please contact Louwrens Koen Attorneys.

Antenuptial Contracts – To Sign or Not to Sign?

Louwrens Koen Attorneys provides expert guidance on Antenuptial Contracts (ANCs) in South Africa. Family Law,

When it comes to Antenuptial Contracts (ANCs), it is important to understand their significance and what they entail. This document may be just as important as your last will and testament in many cases. In this article, we aim to provide an overview of an ANC and its implications for those who choose to sign it in South Africa. An ANC is a contract between future spouses that regulates several aspects of their marriage, including:

- Exclusion of assets owned prior to the marriage;

- Determination of the commencement value of the estate;

- Division and calculation of the estate upon divorce, including an accrual claim or not;

- Transactions with third parties during and after a divorce;

- Distribution of assets upon divorce and death.

Under South African law, an ANC determines the marriage regime under which the couple will fall into. There are three types of regimes:

- Community of Property – where there is no ANC, and all assets and liabilities are jointly owned and equally shared between the spouses.

- Out of Community of Property with the application of the accrual system – where each spouse declares their nominal value at the start of the marriage and retains their assets and liabilities until death or divorce. The accrual of each spouse's assets and liabilities is then calculated and divided.

- Out of Community of Property with no accrual system – where the assets and liabilities of each spouse are separate and not shared, with a potential claim for spousal maintenance.

It is crucial to have a full understanding of the implications of each regime before signing an ANC. It is also important to note that an ANC is a contract, and both parties must fully understand and agree to its terms for it to be considered valid. For any questions regarding the drafting of an ANC, please contact Louwrens Koen Attorneys.

Antenuptial Contracts: With or Without the Accrual System?

Antenuptial contracts (ANCs) determine the financial status of a marriage - whether it will be in community of property or out of community of property, with or without the accrual system.

It must be signed by the marrying couple, two witnesses, and a notary public, then registered in the Deeds Registries office within the required timeframe.

The accrual system calculates how much the spouse with the larger estate must pay the spouse with the smaller estate if the marriage ends through death or divorce. It only takes into account property acquired during the marriage. Without the accrual system, each spouse keeps their own estate, consisting of property and debts acquired prior to and during the marriage, with nothing shared between them. The accrual system is based on the idea that each spouse should take out the value of assets they brought into the marriage and share what they built together during the marriage. However, it only applies if the marriage ends and cannot be claimed while the couple is still married.

Whether to include the accrual system in the ANC is a decision left to the couple, but it is crucial that they consult with a neutral and professional lawyer who can advise and mediate the agreement.

Emotions and personal biases can affect the outcome, especially if one spouse has significantly more assets than the other. Please note that this article is for informational purposes only and should not be used or relied upon as legal or professional advice.

Contact Louwrens Koen Attorneys for specific and detailed advice.

What You Need to Know About Excluding Assets from the Accrual System in Your Antenuptial Contract

The accrual system is a matrimonial property regime that allows spouses to share the growth of their estates during the marriage, without joining their separate estates. The accrual is calculated by subtracting the net value of each spouse’s estate at the commencement of the marriage from the net value of each spouse’s estate at the dissolution of the marriage.

The spouse with the smaller or no accrual has a claim against the other spouse for half of the difference between their accruals1. Some spouses may choose to exclude certain assets from the accrual system in their antenuptial contract. This means that those assets will not be considered as part of their estates when calculating the accrual.

The reasons for excluding assets may vary depending on the circumstances of each case, but some possible reasons are:

To protect a specific asset that has been promised to a third party, such as a family member or a beneficiary of a trust. To retain the income derived from a share in a family business or a trust, without sharing it with the other spouse.

To avoid the risk of losing a speculative asset that may generate significant capital profits, such as a property or a stock.

To preserve the value of an asset that has sentimental or personal value, such as an inheritance, a donation, or a personal injury claim.

Excluding assets from the accrual system may have advantages or disadvantages for the spouses, depending on the outcome of the marriage and the value of the assets. Therefore, it is important to consult a legal professional before entering an antenuptial contract and to make informed decisions about the exclusion of assets.